Article-At-A-Glance: What You Need to Know About Aurum Before Reading Further

Before we go deeper, here are the main points worth holding in mind:

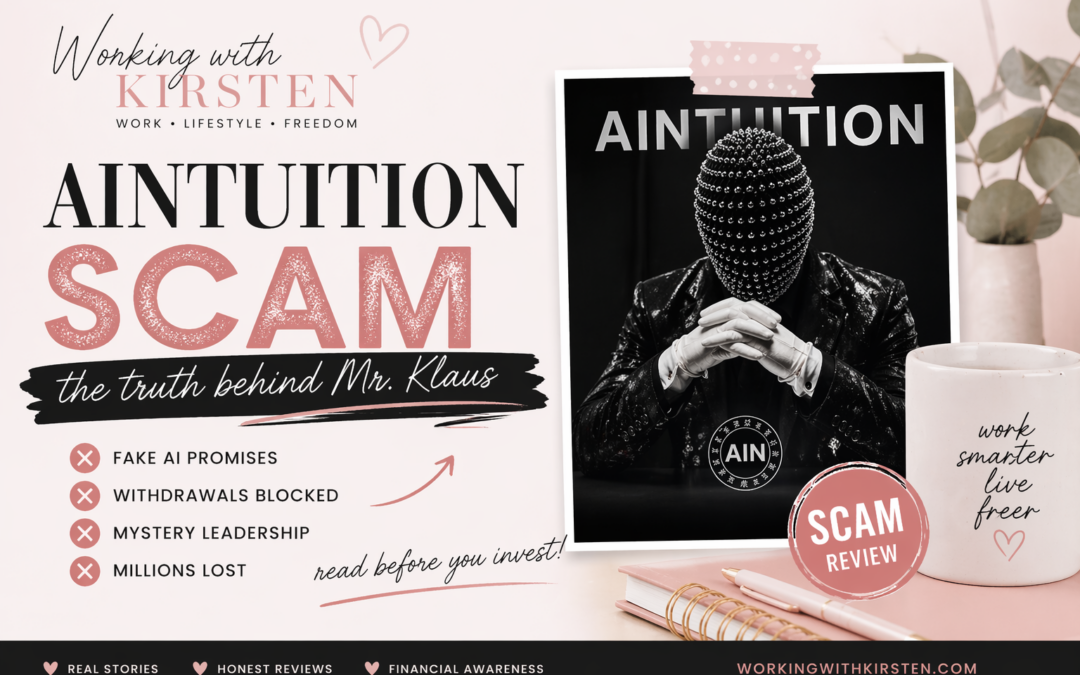

Aurum Foundation claims $30 million in assets under management and 18,000+ active partners — but verifying those numbers through independent sources is harder than it should be.

The platform promotes five tech products including AI trading bots, a NeoBank, crypto cards, an exchange, and gold/XAU packages — a wide product suite that raises questions about focus and sustainability.

Several online communities, including Reddit threads, have raised concerns comparing Aurum’s structure to known crypto recruitment schemes — not proof of wrongdoing, but worth knowing before you commit capital.

A polished website and confident leadership claims are not substitutes for audited financials — and the difference between the two is exactly what this guide unpacks.

Keep reading to find out the five questions every serious investor should ask before trusting any platform like Aurum with their money — including one question most people never think to ask.

The most important question is not whether Aurum looks exciting, but whether the claims behind it can be checked calmly, independently, and without relying on emotion.

In 2026, the most dangerous financial opportunities no longer look dangerous at all.

They arrive with sleek branding, AI-forward language, passive income promises, and leadership teams that name-drop major players in the crypto industry. Aurum Foundation is one such platform that has been generating significant buzz — and significant skepticism — across online financial communities. This guide is not here to tell you what to think. It is here to give you the tools to think clearly. For more resources on navigating financial decisions with confidence, WorkingWithKirsten.com provides ongoing guidance and insight for everyday investors trying to cut through the noise.

My Personal Experience & Honest Perspective

One reason I write articles like this is because I understand how emotionally charged financial decisions can become.

Many people online speak as if everyone makes decisions in a perfectly logical, detached, spreadsheet-style way. Real life is not like that. People make decisions while managing bills, uncertainty, family responsibilities, disappointment, hope, ambition, and the desire to finally get ahead.

I understand that reality deeply.

Over the years, I have seen opportunities that looked extraordinary on the surface but felt very different once time passed and more information emerged. I have also seen that not every unconventional path should be rejected simply because it is unfamiliar. Sometimes there are genuine opportunities hidden beneath skepticism, just as there can be serious risks hidden beneath beautiful branding.

That is why I no longer approach opportunities from excitement alone or cynicism alone.

I approach them with maturity.

I look for patterns. I pay attention to leadership. I observe whether people are being educated or merely emotionally sold. I ask whether the culture encourages responsibility or dependency. I notice whether transparency grows over time or becomes harder to access.

That perspective is what shaped this article.

My intention is never to tell readers what to do. My intention is to help people slow down enough to think for themselves, because thoughtful independence is far more valuable than blindly following promoters or blindly following critics.

If Aurum turns out to be a meaningful opportunity for some people, excellent. If it turns out not to be the right fit, that is equally fine. The true win is not forcing a yes or no answer. The true win is becoming the kind of person who can evaluate opportunities wisely.

And in today’s world, that kind of discernment may be one of the greatest assets anyone can build.

When Financial Opportunities Start Looking Beautiful

There was a time when questionable financial opportunities were easier to recognize.

They often arrived looking unfinished, rushed, or almost too obviously unrealistic. The language was clumsy, the promises were exaggerated, and the presentation itself gave people a reason to hesitate.

But the online world has changed.

Today, a financial platform can arrive beautifully packaged. It can have a sleek website, a modern logo, polished videos, carefully chosen words, and a confident message about innovation, artificial intelligence, passive income, and financial freedom. It can sound intelligent. It can look professional. It can feel, at first glance, like something serious.

That is why platforms like Aurum Foundation deserve a more thoughtful look.

Not because every polished platform is automatically suspicious, but because polish alone can no longer be used as proof of credibility. In 2026, the line between innovation and marketing can feel very thin, especially when people are tired, financially stretched, and looking for a way to create more breathing room in their lives.

This article is not written to tell you what to think. It is written to help you slow down, ask better questions, and separate presentation from proof.

Aurum Foundation Claims $30M AUM and 18,000 Partners — Here Is What That Actually Means

When a platform leads with headline numbers, those numbers are doing a job — and that job is building trust quickly. Aurum Foundation promotes $30 million in assets under management, 18,000+ active partners, and five launched tech products as proof of its legitimacy and scale. These are compelling figures. But compelling and verified are two very different things.

Assets under management, or AUM, is a standard financial metric used by regulated firms like hedge funds, wealth managers, and ETF providers. When a regulated firm reports AUM, that figure is subject to oversight, auditing, and legal accountability. When an unregulated or loosely regulated platform uses the same language, the number may reflect something far less structured — including user deposits that have not been independently verified or audited by a third party.

The 18,000+ active partners figure is similarly worth examining. The word partners is doing a lot of work here. In multi-level or affiliate-driven financial platforms, “partners” often means recruiters or affiliates — people who earn by bringing others in — rather than institutional investors or professional financial actors. That distinction matters enormously when you are trying to assess whether a platform has real market traction or just effective recruitment.

What Aurum Foundation Says It Is

Aurum Foundation presents itself as a fintech company operating at the intersection of artificial intelligence, cryptocurrency, and traditional financial services. Their public-facing materials describe a global operation with international licensing, a technology-first philosophy, and a mission centered on financial inclusion and wealth creation. The framing is modern, aspirational, and carefully constructed to appeal to people who feel left behind by traditional banking systems.

According to their promotional content, Aurum positions itself as more than just an investment platform — it frames itself as an ecosystem. That word, ecosystem, is increasingly common in crypto and fintech marketing because it implies interconnection, self-sustainability, and long-term value. Whether the underlying business actually functions as a cohesive ecosystem or simply markets itself as one is a question that requires deeper investigation than a homepage can answer.

Aurum’s product suite, as promoted publicly, includes AI trading bots, a NeoBank offering, crypto debit cards, a cryptocurrency exchange, and gold or XAU-backed investment packages. More recently, AI agents have also been mentioned in affiliated promotional materials. On the surface, this is an ambitious lineup — one that would place Aurum in competition with established players in each of those verticals simultaneously.

That breadth is worth flagging. Building one credible fintech product takes significant capital, regulatory compliance, and technical infrastructure. Building five — plus an exchange — simultaneously, while also running a global partner recruitment program, raises legitimate questions about resource allocation and operational maturity. Established firms like Coinbase or Revolut spent years and hundreds of millions of dollars building out individual product lines before expanding. The timeline and funding behind Aurum’s multi-product rollout has not been publicly documented to the same degree.

Leadership Claims and the Binance Connection

One of the more notable claims circulating in Aurum’s promotional materials is a connection to Binance — specifically, references to former Binance strategic partner involvement at the leadership level. Names like Bryan Benson, Drei Menza, and Leonardo Galindez have appeared in affiliated content, with Galindez in particular referenced in connection to Binance activity. It is important to note that being a former strategic partner of, or having worked adjacent to, Binance does not constitute an endorsement from Binance — nor does it verify the legitimacy of a separate venture. Binance itself has not publicly affiliated with or endorsed Aurum Foundation based on available information.

Why People Feel Drawn to Platforms Like Aurum

Understanding why intelligent people get drawn into high-risk or unverified financial platforms is not about condescension — it is about context. The economic environment of the mid-2020s has created a near-perfect psychological storm for platforms like Aurum to thrive in.

The Emotional Pull of Passive Income Promises

Passive income is one of the most emotionally resonant phrases in personal finance. It speaks directly to a desire that is both completely understandable and deeply human — the desire to earn without being trapped in a cycle of trading time for money. When a platform presents passive income not as a distant goal but as an immediate, accessible product, the emotional response can override the analytical one.

Aurum, like many platforms in this space, frames its offerings in language that makes passive income feel not only possible but imminent. AI trading bots that work while you sleep. Gold-backed packages that grow automatically. NeoBank features that optimize your holdings. Each product speaks to a version of financial freedom that resonates — and that resonance is a powerful marketing tool, regardless of whether the underlying mechanics support the promise.

How Rising Costs and Job Fatigue Make People Vulnerable

The cost of living increase across most developed and developing economies has pushed millions of people to look for income streams outside their primary employment. When rent, groceries, and energy costs rise faster than wages, the mental bandwidth available for careful financial due diligence shrinks — and the appeal of a simple, high-return solution grows disproportionately.

Job fatigue compounds this. People who are exhausted by demanding, low-reward work are not approaching investment decisions from a place of calm, analytical clarity. They are approaching them from a place of urgency and hope. Platforms that understand this — whether intentionally or not — tend to design their messaging accordingly: urgency cues, limited-time offers, community belonging, and the promise of a fundamentally different financial life.

This is not unique to Aurum. It is the operating environment that every high-yield, network-adjacent financial platform operates within right now. Recognizing that environment is the first step to making decisions that are driven by evidence rather than emotion.

Fear of Missing the Crypto Wave

FOMO — fear of missing out — has been one of the most documented behavioral drivers in crypto investment cycles. The narrative that early Bitcoin adopters became millionaires has created a lasting cultural belief that the next transformative crypto opportunity is always just around the corner, and that hesitation equals permanent loss. Platforms like Aurum are fluent in this narrative, positioning entry into their ecosystem as a time-sensitive opportunity in a rapidly evolving market.

What Public Information Actually Shows

Separating what Aurum claims from what can be independently confirmed is the most important analytical exercise any prospective participant can do. Marketing language and public record are rarely the same document.

What is publicly observable includes the platform’s promotional websites and affiliated social content, testimonials from self-identified members, and discussion threads on platforms like Reddit where users have openly compared Aurum’s structure to recruitment-heavy schemes. What is notably absent from the public record — as of available research — includes independently audited financial statements, verifiable regulatory licensing documentation from named jurisdictions, and transparent corporate registration details that trace clear ownership and legal accountability.

Verifiable Claims vs. Marketing Language

The gap between what a financial platform claims and what it can prove is where real risk lives. Aurum’s public materials are rich with impressive-sounding metrics — $30 million AUM, international licenses, AI-powered infrastructure — but none of these claims have been substantiated through independently audited reports or verifiable regulatory filings available to the public. That absence is not automatically proof of fraud. It is, however, proof of a transparency deficit that any serious investor should weigh carefully.

When legitimate financial institutions make claims about assets under management or regulatory compliance, those claims come attached to documentation — annual reports, FCA registrations, SEC filings, AMF authorizations. The existence of that documentation is not a formality. It is the mechanism through which accountability is enforced. Platforms that use the same language as regulated institutions without the same documentation are borrowing credibility they have not formally earned.

Aurum Foundation Compensation Plan Explained

Perhaps the most structurally significant thing to examine in any network-adjacent financial platform is how money actually flows through the compensation plan. When a platform rewards recruitment as aggressively as it rewards investment performance — or more so — the revenue model begins to resemble a structure where earlier participants are sustained by the capital of newer ones. That is the defining characteristic regulators look for when investigating pyramid or Ponzi-adjacent schemes.

Key Structural Red Flags in Network-Based Financial Platforms:

• Recruitment bonuses that match or exceed trading returns — When the fastest path to earnings is bringing in new members rather than investment performance, the business model is recruitment-dependent by design.

• Tiered commission structures — Multiple levels of commissions paid upward through a recruitment chain are a hallmark of MLM compensation design, not traditional fintech.

• Vague return attribution — If the platform cannot clearly explain which specific trading activity, product, or financial instrument generated a given return, that is a meaningful gap.

• Lock-in periods tied to rank advancement — Requiring members to maintain or upgrade membership levels to access earnings creates structural pressure to reinvest rather than withdraw.

• Income disclosure statements absent — Legitimate MLM and network companies in regulated markets are often required to publish income disclosure statements showing average earnings across all participant levels. The absence of this document speaks volumes.

Aurum’s compensation plan, based on publicly available promotional content, includes tiered partner levels and referral-based incentives. The specific mechanics — how returns are calculated, what percentage flows from trading versus membership fees versus recruitment — have not been transparently disclosed in a standardized format. That makes it structurally difficult to determine whether the model is investment-led or recruitment-led.

This is not a minor distinction. An investment-led model generates returns from real market activity and can sustain itself without continuous recruitment. A recruitment-led model requires constant new member acquisition to maintain payouts — and when recruitment slows, the structure becomes financially unstable. Knowing which type of model you are participating in before you commit capital is not optional due diligence. It is the most important question you can ask.

Community Reactions and Skepticism Already Online

Public skepticism about Aurum Foundation is not difficult to find. Reddit threads — particularly in communities focused on crypto and MLM awareness — have featured open discussions comparing Aurum’s structure to patterns seen in previous high-profile crypto recruitment schemes. Users have raised specific concerns about withdrawal delays, the dominance of recruitment in the income model, and the difficulty of verifying leadership credentials independently. It is important to note that online forum commentary is not definitive evidence of wrongdoing — but it is a meaningful signal that warrants attention.

The volume and consistency of skeptical commentary matters here. When isolated users express doubt, it may reflect personal experience or misunderstanding. When skepticism appears repeatedly, across multiple independent communities, citing similar structural concerns, that pattern deserves serious weight. Due diligence means reading both the testimonials on the official website and the threads where former or questioning participants share their unfiltered experiences.

🌿Want More Honest Opportunity Reviews?

If reflections like this resonate with you, you may enjoy the Working With Kirsten newsletter, where I occasionally share deeper thoughts about building a meaningful online lifestyle, navigating digital communities, and creating environments that encourage curiosity and personal growth.

Inside the newsletter, I often expand on many of the themes explored here on the blog — including the evolving culture of the online world, the importance of thoughtful communities, and the small habits that quietly shape how life feels from day to day.

✨ Reflections on building a thoughtful internet lifestyle 🌱 Insights on personal growth and digital communities ☕ Behind-the-scenes perspectives from my own journey online

If these ideas interest you, you’re always welcome to join the conversation.

No noise. Just thoughtful ideas and quiet reflections about building a life that feels genuinely rich.

5 Questions I Would Ask Before Trusting Any Platform Like Aurum

Before trusting any online financial platform with money, I would want clear answers to these five questions.

1. How exactly are returns generated?

“AI trading” is not enough of an answer.

A serious platform should be able to explain what markets are being traded, what strategies are used, who oversees the process, how risk is managed, and whether performance has been independently verified.

If the answer is vague, overly technical, or hidden behind marketing language, that is a reason to pause.

2. Are the claimed returns realistic?

Any platform that suggests unusually strong, consistent, or predictable profits deserves extra scrutiny.

Markets move. Trading involves risk. Even experienced professionals experience losses, drawdowns, and volatility.

When returns sound too smooth, too high, or too certain, the question is not whether we want them to be true. The question is whether they can be proven.

3. Which regulators can verify the licenses?

Licensing language can sound reassuring, but it must be specific.

A serious due diligence process should include checking the official public registers of relevant regulators. If a company claims licensing or authorization, you should be able to find the regulator, license number, jurisdiction, and exact legal entity.

Registration is not always the same as regulation.

And regulation in one jurisdiction may not protect customers in another.

4. Is the income model based on financial activity or recruitment?

This is one of the most important questions of all.

If most income comes from trading, banking services, exchange fees, or legitimate product use, that points in one direction.

If most income appears tied to new memberships, rank advancement, referral bonuses, or package sales, that points in another.

The difference is not small. It goes to the heart of sustainability.

5. What happens when people withdraw larger amounts over time?

Early withdrawals can create trust, but they do not always prove long-term stability.

The more useful evidence comes from people who have been involved for longer periods and have withdrawn meaningful amounts without delays, excuses, changing rules, or added conditions.

A platform should be judged not only by how easy it is to join, but by how cleanly people can leave.

Why a Beautiful Website Is Not the Same as an Audit

There is a cognitive shortcut that most people rely on when evaluating unfamiliar organizations — and it is increasingly unreliable. When something looks professional, modern, and technically sophisticated, the brain interprets that as a signal of legitimacy. In previous decades, building a credible-looking financial platform required significant capital and infrastructure. Today, a convincing website, a polished explainer video, and a professionally designed whitepaper can be assembled for a fraction of that cost — and none of it constitutes financial accountability.

An audit, by contrast, is a formal examination of a company’s financial statements and records by an independent, qualified third party. It involves verification of actual transactions, account balances, and financial flows against documented evidence. No amount of design quality, AI language, or leadership credentials substitutes for that process. When evaluating Aurum — or any platform making significant financial claims — the single most clarifying question you can ask is: where is the independently audited financial statement? If that document does not exist or is not made available, everything else on the website is marketing.

Polished Branding vs. Financial Transparency

Aurum’s digital presence is undeniably well-constructed. The website uses clean design language, professional photography, and the kind of confident, forward-looking copy that signals competence to a casual visitor. But visual sophistication and financial transparency are not the same thing — and conflating them is one of the most common and costly mistakes individual investors make when evaluating emerging platforms.

Financial transparency has a specific meaning. It means audited accounts, published risk disclosures, verifiable licensing, clear ownership structures, and documented performance records that have been reviewed by parties with no financial interest in making the numbers look good. None of those elements can be communicated through a homepage hero image or a slick product demo video. When you strip away the visual layer of any financial platform and ask what verifiable documentation remains, you get a much clearer picture of what you are actually dealing with.

The Pattern of Marketing Outpacing Accountability

Aurum is far from alone in this pattern. Across the crypto and alternative finance space, marketing infrastructure consistently outpaces compliance infrastructure — because marketing generates momentum and momentum generates recruitment, while compliance generates costs and friction. The platforms that collapse most publicly are almost always the ones where the brand was built faster than the business. Promises scaled faster than infrastructure. Community grew faster than governance.

The warning sign is not the quality of the marketing. The warning sign is the absence of accountability structures that should exist alongside it. A platform with genuine institutional backing, real trading performance, and verifiable regulatory standing has every incentive to lead with that documentation — because it is the strongest possible trust signal available. When that documentation is consistently absent, replaced instead by testimonials, lifestyle imagery, and recruitment incentives, the gap itself becomes the most important data point.

My Personal View on Aurum in 2026

After spending time researching Aurum, looking at the public-facing materials, reviewing the language used in promotions, and considering the wider online conversation surrounding the platform, my view is a balanced one.

I do not believe people should approach Aurum with blind excitement, but I also do not believe every emerging opportunity should be dismissed simply because it is modern, crypto-based, or uses referral structures. Many people make the mistake of living at one extreme or the other. They either trust too quickly because something looks polished, or they reject too quickly because something is unfamiliar.

A wiser position usually sits somewhere in the middle.

Aurum appears to be a platform with ambition, momentum, and a vision built around alternative finance, technology, and community growth. For some people, that may feel aligned with where the future is heading.

For others, the lack of traditional structure, public familiarity, or easily accessible documentation may create hesitation. Both responses are understandable.

My honest view is that Aurum may be worth exploring for people who understand the risks, do their own due diligence, and approach it responsibly rather than emotionally. It should not be treated as a guaranteed solution, nor as something to join under pressure or because someone else appears excited.

It should be approached the same way any higher-risk emerging opportunity should be approached: thoughtfully, carefully, and with full personal responsibility.

For readers who are curious, financially disciplined, and comfortable learning as they go, Aurum may be worth researching further as part of a broader strategy rather than as a single answer to everything.

My Final Verdict on Aurum – Is Aurum Foundation Legit?

Aurum appears to be a modern opportunity that may appeal to people interested in crypto, technology, community-based growth, and alternative ways of building income outside traditional systems. It is not something I would frame as “easy money,” nor something I would suggest entering carelessly. However, for the right person — someone who understands risk, starts modestly, and remains grounded — it may be worth considering.

I would personally view Aurum as an opportunity to explore, not a certainty to depend on.

That distinction matters greatly.

If you decide to look into it, I would recommend:

Start small and stay sensible.

Never use money needed for essentials.

Learn the platform rather than rushing in.

Build slowly instead of emotionally.

Diversify rather than relying on one source.

Stay alert, informed, and personally accountable.

Sometimes the best opportunities are not found through hype, but through patient observation and disciplined action over time.

In Today’s World, the Real Danger Looks Beautifully Credible

The financial threats that defined previous generations were easier to spot. Bad grammar in cold emails. Pressure calls from unknown numbers. Promises that arrived without polish or plausibility. The threats that define this generation are different. They arrive with professional design teams, AI-powered product suites, and leadership figures who speak fluently in the language of innovation and disruption.

That shift does not mean every polished platform is dangerous — it means the visual presentation of a platform can no longer be used as a proxy for its safety or legitimacy. The real danger in 2026 is not something that looks suspicious. It is something that looks exactly like what trustworthy financial innovation is supposed to look like — right up until the moment it does not. The only reliable protection against that is disciplined, documentation-first due diligence, every single time, with no exceptions made for compelling branding or persuasive community energy.

Why This Matters Beyond Aurum

Although this article focuses on Aurum, the deeper lesson reaches far beyond one platform or one company. We are living through a period where millions of people are rethinking how they earn, save, invest, and create security for themselves. Traditional systems no longer feel as dependable to many households as they once did, and because of that, people are naturally exploring new paths.

That search for alternatives is not foolish. In many ways, it is rational. People want flexibility, more control over their income, and opportunities that reflect the digital age rather than outdated financial models. They want to believe there are still doors open for ordinary people who are willing to learn and take action.

The challenge is that genuine innovation and aggressive marketing often exist side by side. Some platforms truly are building something valuable, while others may simply be selling the appearance of progress. Telling the difference requires patience, emotional discipline, and a willingness to look deeper than surface presentation.

That is why articles like this matter. They are not about fear. They are about discernment. They are about helping everyday people make decisions from a place of clarity rather than urgency. They are about remembering that financial wellbeing is usually built through steady thinking, not rushed reactions.

Whether someone chooses Aurum, another platform, or none at all, the real goal should always be the same: to make thoughtful decisions that protect long-term peace, preserve dignity, and create options for the future.

Questions Worth Asking Before Joining Any Financial Opportunity Like Aurum

Before joining any platform, ask yourself:

Do I understand how money is actually made here?

Is the model sustainable without constant new people joining?

Would I still feel confident if no one else was promoting it?

Am I acting from clarity or from urgency?

Would I be comfortable explaining this decision to my future self?

Those questions alone can save people from many expensive mistakes.

Explore Aurum for Yourself

If Aurum resonates with you and you would like to research it personally, there is nothing wrong with taking a closer look and making your own informed decision.

Sometimes the smartest path is not to follow noise from either side, but to quietly study, ask questions, and decide based on your own judgment.

As always, I encourage readers to do their own research, move responsibly, and never invest more than they can comfortably afford to lose.

More Resources & Recommended Reading

For readers who want to become wiser, calmer, and more independent when evaluating money decisions, online opportunities, and modern wealth-building claims, I always believe books can be one of the best investments a person makes. A strong book can save you years of confusion, costly mistakes, and emotional decision-making.

These are titles I would genuinely recommend reading, along with why each one matters.

1. The Psychology of Money – The Psychology of Money

This is one of the most valuable modern books on wealth because it explains that money decisions are rarely about spreadsheets alone. They are often shaped by emotion, ego, fear, impatience, insecurity, and personal history. If someone wants to understand why people chase risky opportunities or panic during uncertainty, this book offers beautiful perspective.

Why I recommend it: Because financial success is often less about intelligence and more about behavior, patience, and emotional steadiness.

2. Thinking, Fast and Slow – Thinking, Fast and Slow

This book explores how the human mind makes decisions through two systems: fast emotional thinking and slower rational thinking. It helps readers understand why urgency, hype, fear of missing out, and social proof can influence judgment without us realizing it.

Why I recommend it: Because anyone researching platforms like Aurum should understand how easily emotion can disguise itself as logic.

3. Influence – Influence

A classic book on persuasion and why people say yes. It covers principles such as authority, scarcity, reciprocity, consistency, and social proof — all tactics often used in marketing, recruiting, and sales environments.

Why I recommend it: Because once you understand persuasion psychology, you become far harder to manipulate.

4. The Millionaire Fastlane – The Millionaire Fastlane

This book challenges traditional beliefs about wealth-building and explores entrepreneurship, leverage, scale, and creating value rather than simply exchanging time for money. While bold in tone, it offers useful mindset shifts for readers wanting alternatives to the standard path.

Why I recommend it: Because it encourages readers to think creatively about income rather than believing there is only one road to financial progress.

5. Rich Dad Poor Dad – Rich Dad Poor Dad

Though widely known and sometimes debated, this book helped many people begin thinking differently about assets, liabilities, financial education, and building income streams outside employment.

Why I recommend it: Because even when readers do not agree with every point, it often awakens a deeper curiosity about money.

6. Atomic Habits – Atomic Habits

Many people search for financial breakthroughs while ignoring the daily habits that create long-term results. This book explains how tiny repeated improvements compound into meaningful change over time.

Why I recommend it: Because wealth is often built quietly through habits long before it is seen publicly.

7. The Richest Man in Babylon – The Richest Man in Babylon

A timeless classic written through simple parables, teaching principles such as saving first, living below your means, and letting money grow wisely over time.

Why I recommend it: Because old wisdom often remains relevant, especially in a world obsessed with shortcuts.

8. Your Money or Your Life – Your Money or Your Life

This book invites readers to rethink their relationship with money, consumption, work, and what a meaningful life truly looks like. It is especially valuable for people who feel trapped in endless earning without deeper fulfillment.

Why I recommend it: Because not every financial goal should be measured only by numbers. Lifestyle matters too.

A Personal Note on Reading

Whenever I research opportunities like Aurum, I often notice that many people are searching for a shortcut when what they may need most is stronger financial thinking.

A good book may not promise instant returns, but it can quietly build discernment, patience, confidence, and independence — qualities that often become far more profitable over a lifetime than chasing every new opportunity.

Sometimes the smartest investment is not the platform you join next.

Sometimes it is the wisdom you build first.

Continue Exploring These Ideas

If you would like to learn more about how certain online financial opportunities can imitate existing platform concepts while repeating familiar pressure-based patterns, you may also find my deeper scam-awareness reflections helpful.

It is a useful companion read because the lesson is not only about one platform or one person. It is about learning how to notice patterns, ask better questions, and protect your peace before trusting any online promise with your time, money, or reputation.

Final Conclusion

After looking at Aurum through a thoughtful and balanced lens, I believe the most sensible conclusion is neither blind enthusiasm nor automatic dismissal.

Too often, people are encouraged to think in extremes when it comes to online opportunities. A platform is either presented as the greatest thing ever created, or condemned instantly without nuance. Real life is rarely that simple. Many modern companies exist somewhere in the middle — containing genuine potential, unanswered questions, strengths, risks, and room for growth all at once.

Aurum appears to be one of those cases.

It may appeal to people who are interested in cryptocurrency, emerging finance, digital ecosystems, and alternative ways of creating income beyond traditional employment. It also raises the kind of questions that any careful person should ask before committing capital, time, or trust.

That is why my final position remains grounded: Aurum may be worth exploring, but it should be explored intelligently.

The wisest path is never emotional urgency. It is calm evaluation.

Take time to understand the model. Learn how the platform works. Verify what you can. Begin modestly if you choose to participate. Stay responsible. Keep expectations realistic. Protect your essentials. Maintain personal accountability.

Financial wellbeing is rarely built through panic, pressure, or fantasy. More often, it is built through steady decisions made over time.

Whether Aurum becomes a meaningful opportunity for some people or not, the larger lesson remains valuable: in the modern online world, the ability to think clearly is one of the most profitable skills anyone can develop.

Aurum Foundation FAQ

Below are the most common questions people ask when researching Aurum Foundation — answered directly, without spin, based on what the available public record actually supports.

Is Aurum Foundation a Legitimate Investment Platform?

Based on publicly available information, Aurum Foundation has not provided the level of documented, independently verified evidence that would allow a definitive answer in either direction. What can be assessed are the observable characteristics of the platform against the benchmarks used to evaluate financial legitimacy. Those benchmarks include:

Independent audits: No publicly available independently audited financial statements have been identified.

Regulatory verification: Licensing claims have not been confirmed through publicly searchable regulatory databases of major jurisdictions.

Revenue model clarity: The balance between trading revenue and recruitment-based revenue has not been transparently disclosed.

Withdrawal consistency: Long-term withdrawal reliability across a broad participant base has not been independently documented.

Corporate transparency: Clear, traceable corporate registration and ownership structure information is not readily available through public records.

Each of these gaps does not independently prove illegitimacy. Together, they represent a pattern of opacity that distinguishes Aurum from platforms that have earned verifiable trust. Absence of proof is not proof of absence — but it is a legitimate reason for caution before committing capital.

If you are actively considering participation, the minimum acceptable step before proceeding is engaging an independent financial advisor who has no connection to the platform and asking them to review whatever documentation Aurum provides. Their assessment — not the platform’s promotional materials — should anchor your decision.

What Is Aurum Foundation?

Aurum is a decentralized fintech company, dedicated to the development of innovative crypto products and ai-powered algorithms that redefine how users manage and grow their digital assets.

Aurum offers a secure and efficient ecosystem where contribute capital, payments, and trading come together seamlessly, empowering both individuals and businesses to achieve their financial goals.

What Licenses Does Aurum Foundation Hold and Are They Verifiable?

Aurum’s promotional materials reference international licensing, but specific regulatory bodies, license numbers, and jurisdictions have not been publicly confirmed through verifiable independent sources as of available research. To check this yourself, search the public registers of the FCA (UK), SEC (USA), AMF (France), ASIC (Australia), and any other jurisdiction Aurum claims authorization in. Enter the company name and any associated entity names directly into those official databases. If the registration does not appear — or appears only under a low-scrutiny offshore registration — treat any licensing language in Aurum’s marketing materials with significant skepticism.

How Does the Aurum Foundation Compensation Plan Work?

Based on available promotional content, Aurum’s compensation plan includes tiered partner levels with referral-based incentives — meaning participants can earn commissions by recruiting new members into the platform. The specific percentages, tier thresholds, and the ratio of recruitment earnings to trading-based earnings have not been published in a standardized, auditable format. This structure is broadly consistent with multi-level marketing compensation design rather than traditional investment platform fee structures. Whether the recruitment component is incidental or central to the economic model is a question Aurum has not answered transparently in publicly available materials.

What Do Reddit and Online Communities Say About Aurum?

Online communities — particularly Reddit threads focused on cryptocurrency, passive income, and MLM awareness — contain multiple discussions questioning Aurum Foundation’s legitimacy. Common themes include concerns about recruitment pressure outpacing investment substance, reported difficulties with withdrawal processes over time, skepticism about the Binance connection claims, and comparisons to structural patterns seen in previous crypto platforms that ultimately collapsed. These community observations are not legal findings, and individual experiences vary. However, the consistency and geographic spread of skeptical accounts across unaffiliated forums is a signal that warrants serious attention.

It is equally important to note that Aurum has active advocates and promoters in online spaces who report positive early experiences. Positive early experiences — particularly around initial withdrawals — are common even in platforms that later encounter structural problems. Weigh the full range of community commentary, prioritizing long-term participant accounts over those from recent joiners with limited platform history.

What Should I Do Before Investing in Any Platform Like Aurum?

Pre-Investment Due Diligence Checklist — Use This Before Committing Any Capital

Due Diligence Step

What to Look For

Red Flag If…

Verify regulatory licenses

Search official regulator databases directly

Company does not appear or is only offshore-registered

Request audited financials

Ask for independently audited annual statements

None exist or access is refused

Analyze the compensation plan

Identify ratio of trading income vs. recruitment income

Recruitment earnings dominate the income model

Research withdrawal history

Find accounts from 12+ month participants

Withdrawal conditions have changed or delays are reported

Repeated structural concerns from diverse, independent sources

Start with the regulator search. It costs nothing, takes under five minutes, and immediately tells you whether the platform’s licensing claims hold up against the public record. This single step eliminates a significant proportion of illegitimate platforms without requiring any financial expertise.

Next, request documentation directly from Aurum. Ask specifically for independently audited financial statements, the full compensation plan with income disclosure data, and the license numbers with corresponding regulatory bodies. A legitimate platform will provide these without hesitation. A platform that deflects, delays, or responds with promotional materials instead of legal documentation has answered your question through its non-response.

Protect your downside before you calculate your upside. The most common mistake individual investors make with high-yield alternative platforms is spending their analytical energy on calculating potential returns before fully assessing potential losses. The question to ask first is never how much could I make — it is always what happens to my capital if this platform stops operating tomorrow, and what legal recourse would I have? In most cases with unregulated or lightly regulated platforms, the honest answer to that question is: very little.

Never invest capital you cannot afford to lose completely. This is not a disclaimer — it is the foundational principle of rational risk management. If a platform’s promised returns look like they could solve a significant financial problem in your life, that emotional context is precisely what makes the decision dangerous. Financial desperation and sound investment decision-making are structurally incompatible. Make sure any capital you consider allocating to a platform like Aurum is genuinely discretionary — money whose complete loss would not affect your housing, nutrition, debt obligations, or emergency reserves.

Share Your Personal Experience With Aurum

One of the most valuable parts of any financial conversation is hearing from real people who have actually experienced a platform firsthand.

Marketing pages will always highlight the best moments. Promotional videos will naturally focus on the positive side. Critics may focus only on concerns. But genuine reader experiences often provide the most balanced and useful perspective of all.

If you have personal experience with Aurum, I warmly invite you to share it in the comments below. Your story may help someone else make a calmer, more informed decision.

You might consider sharing:

How long you have been involved with Aurum

What first attracted you to the platform

Whether your experience has been positive, neutral, or disappointing

How easy or difficult deposits and withdrawals were

Whether the education, tools, or community felt valuable

If recruitment pressure was present or not

What you wish you had known before joining

Whether you would recommend it to others, and why

Both positive and negative experiences can be helpful when shared honestly and respectfully.

My goal with WorkingWithKirsten.com has always been to create a space where people can learn from one another without hostility, pressure, or unnecessary drama. Real experiences matter, especially in an online world where polished branding can sometimes speak louder than truth.

Please keep comments thoughtful, factual, and respectful of others. Different people may have had very different experiences, and those perspectives can all add value when shared constructively.

Your voice could be exactly what helps another reader pause, reflect, and make a wiser decision.

🌿Want More Honest Opportunity Reviews?

Join my newsletter for calm reviews, scam awareness, and smarter online income ideas.

If reflections like this resonate with you, you may enjoy the Working With Kirsten newsletter, where I occasionally share deeper thoughts about building a meaningful online lifestyle, navigating digital communities, and creating environments that encourage curiosity and personal growth.

Inside the newsletter, I often expand on many of the themes explored here on the blog — including the evolving culture of the online world, the importance of thoughtful communities, and the small habits that quietly shape how life feels from day to day.

✨ Reflections on building a thoughtful internet lifestyle 🌱 Insights on personal growth and digital communities ☕ Behind-the-scenes perspectives from my own journey online

If these ideas interest you, you’re always welcome to join the conversation.

No noise. Just thoughtful ideas and quiet reflections about building a life that feels genuinely rich.

Disclosure

Some of the links in this article may be affiliate links. This means that if you choose to make a purchase through one of these links, I may earn a small commission at no additional cost to you.

I only recommend books, services, products, tools, or communities that I genuinely find interesting, useful, or aligned with the ideas discussed on this site and that I am using myself.

My goal with WorkingWithKirsten.com is to explore thoughtful perspectives on online culture, digital entrepreneurship, and building a more intentional internet lifestyle. Any resources mentioned are shared with the intention of helping readers explore these topics further.

Thank you for supporting this work and for being part of the conversation.

Jordon Schultz’s bankruptcy case turned into a federal legal battle after his former business partner alleged he fraudulently undervalued a customer list worth potentially millions at just $778.60.

The case — Keyword Rockstar, Inc. v. Jordon Schultz — moved through both the Bankruptcy Appellate Panel of the Ninth Circuit and the Ninth Circuit Court of Appeals.

Schultz’s discharge was denied on one key claim, § 727(a)(7), even though he won on several others.

A house fire, custody battle, and mounting legal pressure all became part of the court’s analysis of his mental state and credibility.

The disputed customer list sat at the center of everything: ownership, valuation, and whether the bankruptcy schedules were truthful.

For anyone researching Jordon Schultz today, this is not just old legal history. It is part of a larger credibility record that should not be ignored.

Sometimes the Real Warning Sign Is Not the Sales Page — It Is the Paper Trail

There is something deeply unsettling about realizing that the truth behind a person can be far more complicated than the version most people encounter at first glance.

In the online world, first impressions are often carefully curated. A webinar may feel polished and persuasive. A mentor may speak with confidence and authority. A program can appear professional, structured, and full of promise. The overall presentation may leave people feeling as though they are standing at the threshold of a meaningful opportunity, one capable of changing their finances, their future, or the direction of their lives.

That is precisely why so many people trust appearances before they trust evidence.

Yet there are moments when curiosity leads someone to look beyond the presentation, and what emerges is something altogether different. Instead of a few scattered complaints or an isolated negative review, they uncover court filings, years of litigation, and a legal history that extends far beyond ordinary business friction. They find a dispute that did not quietly fade away, but instead expanded into a bankruptcy battle serious enough to reach the United States Court of Appeals for the Ninth Circuit.

That is why this case matters.

Because no matter how compelling someone may sound in a webinar, on a landing page, or inside a coaching program, public records often tell a steadier and more revealing story. They are less concerned with image and more concerned with facts, timelines, sworn statements, and consequences.

And in this instance, that story deserves to be taken seriously.

Why This Matters More Today

This is not simply a retrospective look at an old bankruptcy dispute. It remains relevant because people continue searching names like Jordon Schultz while trying to decide whether they should trust him, purchase from him, join something connected to him, or understand experiences they may have had themselves.

That is what makes this more than a technical legal article. It sits at the intersection of consumer trust, online business credibility, and the importance of informed decision-making.

When someone’s history includes serious customer complaints, allegations of misleading business practices, rebranded offers, blocked payouts, support problems, and later a federal bankruptcy case involving a denied discharge tied to false valuation issues, readers deserve access to the broader context. They deserve more than a polished sales narrative or the simplified claim that criticism is merely the result of “haters.”

They deserve the full picture.

And in this case, the fuller picture raises important questions about credibility under pressure, accountability when disputes arise, and what it means when a court concludes that a sworn version of events does not withstand scrutiny.

The Jordon Schultz Lawsuit Explained

This was not one simple lawsuit. It was a layered legal conflict that began as a civil dispute in 2015 and evolved into a bankruptcy fraud battle by 2017.

To understand what the courts actually decided, it helps to follow the timeline carefully.

At the center of it all was Jordon Wallace Schultz, the sole owner of JWS Publishing, Inc., a digital content company that sold instructional video products online. By 2016 and 2017, JWS was generating substantial revenue. That mattered later, because the plaintiffs argued that a business generating that kind of income should not have ended up presenting key assets as nearly worthless.

The case is formally known as Keyword Rockstar, Inc. v. Jordon Schultz, No. 19-60031, decided by the Ninth Circuit on June 25, 2020.

Who Is Jordon Schultz?

Jordon Wallace Schultz was the founder and sole owner of JWS Publishing, Inc. His company sold online instructional products and relied heavily on two business assets that later became the focus of the entire bankruptcy fight: a customer list and a lead list.

Those lists were not minor side assets. They were presented as core drivers of revenue. And once the bankruptcy filings placed a surprisingly low value on them, those numbers became one of the biggest credibility issues in the case.

The Core Dispute With Keyword Rockstar, Inc.

Keyword Rockstar, Inc., along with Jon Shugart and Luke Sample, filed an adversary complaint objecting to Schultz’s discharge under multiple provisions of 11 U.S.C. § 727. Their argument was that Schultz had behaved dishonestly in the bankruptcy process.

The allegation that mattered most was this: he had allegedly undervalued JWS’s customer list on the bankruptcy schedules, listing it at $348.60 when it may have been worth dramatically more.

Asset Valuation at the Center of the Case

Asset

Schultz’s Scheduled Value

Plaintiffs’ Argued Value

JWS Customer List

$348.60 ($0.10 per lead)

Up to $1 million

JWS Lead List

$430.00 ($0.02 per lead)

Disputed

Total Scheduled Value

$778.60

Argued to be significantly higher

That gap was not something a court could casually overlook.

And what made it especially difficult for Schultz was that the higher number did not come from nowhere. It came from his own prior public statements.

How the Joint Venture Fell Apart

Before there was a bankruptcy case, there was a business relationship.

Jon Shugart and Jordon Schultz had entered into a 50-50 profit-sharing joint venture. Shugart brought content and expertise. Schultz brought the business infrastructure of JWS Publishing, including access to the customer list.

On paper, that kind of arrangement can look straightforward.

In reality, it unraveled quickly.

What Schultz Discovered in May 2015

In May 2015, Schultz discovered that Shugart had sold copies of JWS video content to contacts on JWS’s customer list without authorization. Shugart described it as testing the strength of the list. Schultz viewed it as an unauthorized use of business assets and a breach of the agreement.

That was the fracture point.

From there, both sides began accusing the other of wrongdoing, and the conflict escalated into litigation.

The Civil Lawsuit Filed in August 2015

In August 2015, Keyword Rockstar, Inc., Jon Shugart, and Luke Sample filed a civil lawsuit against Schultz, JWS Publishing, and others in the U.S. District Court for the Central District of California.

This is important because the story did not begin in bankruptcy. Bankruptcy came later, after the business dispute was already in motion.

And this was not a one-sided case either. Both sides claimed the other owed money. That fact matters because it shows how entangled and contested the business relationship had already become.

The Disputed Ownership of the Customer List

One of the biggest unresolved issues in the civil case was ownership of the customer list itself. Both sides claimed rights to it.

That unresolved ownership issue later became one reason the bankruptcy trustee did not move forward with selling the list during the JWS bankruptcy. If title is under dispute, liquidation becomes far more complicated.

Personal Hardships That Led to Bankruptcy

By the time Schultz filed for bankruptcy in 2017, the lawsuit with Keyword Rockstar had been dragging on for nearly two years.

But the legal dispute was only one layer of pressure.

The 2016 House Fire

In October 2016, Schultz lost his home and its contents in a house fire. That event became part of the court’s understanding of how someone associated with a profitable digital business could still end up in financial collapse.

Child Custody Litigation

At the same time, he was also involved in a child custody battle concerning his infant son. That added another layer of emotional and financial pressure.

Why the Court Considered This

Schultz’s legal team argued that the combination of the house fire, custody battle, medications, and litigation stress affected his mental state and should have weakened any inference of fraudulent intent.

The court considered those arguments.

But in the end, they were not enough to overcome the credibility problems surrounding the valuation issue.

Schultz’s Chapter 7 Filings in 2017

Schultz filed his personal Chapter 7 petition on March 22, 2017.

Seven days later, on March 29, 2017, JWS Publishing filed its own Chapter 7 petition.

That sequence became crucial because the conduct in the JWS case would later be used against him personally under § 727(a)(7).

How the Customer List Was Valued at $778.60

In the JWS bankruptcy schedules, Schultz valued the customer list at $348.60 and the lead list at $430.00, for a combined total of $778.60.

He relied on comparable sales data supplied by his accountant, Benjamin Rucker.

Now, that method itself was not automatically improper. Comparable sales can be a legitimate approach in some contexts.

The problem was the contradiction.

Schultz had also publicly said in a webinar that the customer list was worth $1 million.

That is where the case became especially difficult for him. Courts can tolerate disputes over valuation. What courts struggle to tolerate is a major discrepancy between public claims and sworn filings when the explanation for that discrepancy is not convincing.

Why Plaintiffs Argued the List Was Worth Far More

Keyword Rockstar argued that the list should not be valued using a narrow comparable-sales model when it had allegedly generated millions in revenue.

Their position was that a revenue-generating asset of that size could not credibly be treated as if it were worth less than $800 total.

The court did not have to determine the exact number.

It only had to decide whether the scheduled value was materially false and whether Schultz knew it.

That distinction matters. Bankruptcy courts do not always need a perfect alternate valuation. They need enough evidence to decide whether the number submitted under oath was knowingly misleading.

The Trustee’s Decision to Abandon the Lists

More than a month after JWS filed bankruptcy, the Chapter 7 trustee abandoned the customer list and lead list.

Why?

Because ownership was still being disputed in the ongoing civil litigation, and the trustee did not see a clear path to liquidating assets with unresolved title.

That decision had a ripple effect. Since the lists were not sold, there was no market transaction to establish value. The courts had to rely instead on testimony, public statements, and competing valuation methods.

That left room for argument — but it did not eliminate the core credibility issue.

The Four-Day Bankruptcy Trial

The adversary proceeding went to trial over four days.

Witnesses included:

Jon Shugart

Jordon Schultz

Benjamin Rucker

Susanne Morgan

Joanna Morales

Schultz’s Testimony About His Mental State

Schultz described himself as functioning in a severely diminished state, affected by medications, trauma, and ongoing legal stress. His therapist offered supporting testimony.

But the court did not fully credit that explanation where it counted most.

In the end, this was not just about whether someone was going through a difficult season. It was about whether the court believed the explanation for the numbers in the schedules.

And on that issue, the court found his account lacking.

The Court’s Ruling on Each Claim

This case was not a total loss on every issue for Schultz, and that is worth stating clearly.

He prevailed on several claims.

Claims Where Schultz Won

§ 727(a)(3) — failure to keep adequate records: plaintiffs did not prove it.

§ 727(a)(4)(A) in his personal case — false oath: the Bankruptcy Appellate Panel reversed the bankruptcy court’s finding on that issue.

§ 727(a)(5) — failure to explain loss of assets: plaintiffs did not succeed.

So no, this was not a case where every accusation was upheld.

But that does not change what happened next.

The One Claim That Denied Schultz His Discharge: § 727(a)(7)

This was the claim that changed everything.

Section 727(a)(7) allows a court to deny someone’s personal discharge if they committed a disqualifying act in another bankruptcy case involving an insider.

Since Schultz was the sole owner of JWS Publishing, that insider relationship was clear.

The court concluded that he knowingly and fraudulently undervalued JWS’s customer list in the company bankruptcy. That finding then carried over into his personal bankruptcy through § 727(a)(7).

And that is the claim that survived appeal.

In simple terms: Schultz lost his personal discharge because of what the court found he did in the JWS bankruptcy case.

🌿Let’s Stay Connected & Continue the Conversation…

If reflections like this resonate with you, you may enjoy the Working With Kirsten newsletter, where I occasionally share deeper thoughts about building a meaningful online lifestyle, navigating digital communities, and creating environments that encourage curiosity and personal growth.

Inside the newsletter, I often expand on many of the themes explored here on the blog — including the evolving culture of the online world, the importance of thoughtful communities, and the small habits that quietly shape how life feels from day to day.

✨ Reflections on building a thoughtful internet lifestyle 🌱 Insights on personal growth and digital communities ☕ Behind-the-scenes perspectives from my own journey online

If these ideas interest you, you’re always welcome to join the conversation.

People do not usually search for bankruptcy appellate decisions because they are casually interested in federal procedure. They search because they are trying to decide whether they can trust someone now.

And this case gives them a reason to pause.

Credibility Does Not Reset Just Because Time Passes

If someone publicly describes a customer list as worth $1 million and then schedules it at $348.60 in federal bankruptcy papers, that does not become irrelevant simply because years go by.

A credibility problem on the record is still a credibility problem.

The Pattern Is What Readers Need to Notice

When this case is viewed alongside the other complaints you shared — hidden costs, aggressive coaching funnels, blocked payouts, support that disappears, refund problems, pressure tactics, and repeated rebranding — readers are not looking at one isolated issue.

They are looking at a pattern.

And patterns matter far more than polished branding.

Why You Should Run, Not “See for Yourself”

There is a phrase that appears again and again in the world of online business: Just see for yourself. It is often presented as a sign of confidence, openness, or fairness — as though the only reasonable path is to experience something personally before forming an opinion.

At first glance, that can sound sensible. After all, we are often encouraged to keep an open mind, avoid assumptions, and make decisions based on firsthand experience. In many areas of life, that is wise advice.

But in the context of questionable online offers, high-pressure sales systems, or businesses already surrounded by serious complaints, this phrase can become something very different. It can function less as an invitation to learn and more as a strategy to lower skepticism long enough for someone to pay first and ask harder questions later.

By the time many people “see for themselves,” they have already spent the money, entered the funnel, accepted the emotional pressure, or invested time and trust they cannot easily recover. The lesson is then learned the expensive way.

One of the most valuable forms of maturity in business is recognizing that not every warning must be personally experienced to be valid. Sometimes wisdom looks like research, discernment, and the willingness to walk away before the cost becomes your own.

There are moments in life when curiosity serves us well. There are other moments when discernment matters far more. Knowing the difference can save far more than money.

The Red Flags Are Already Enough

The warning signs are not isolated or incidental, but they form a pattern, and patterns are often where the clearest truth is found.

What emerges repeatedly are concerns such as unrealistic promises, pressure-driven webinars, vague or incomplete transparency, hidden or escalating costs, blocked access, payout issues, refund struggles, and support that appears weak, inconsistent, or absent when it is needed most. Added to that is business conduct serious enough to have resulted in a published federal appellate case.

Any one of these concerns might prompt caution on its own. When several appear together — and continue appearing over time — they deserve to be taken seriously.

At a certain point, a person does not need one more red flag in order to justify stepping back. They need the confidence to trust the ones already in front of them.

Discernment is not cynicism. It is the ability to recognize when enough information has already been provided, and when protecting your time, money, and peace of mind is the wiser decision.

Consistent warning signs to look out for:

unrealistic promises

pressure-heavy webinars

vague transparency

hidden or escalating costs

blocked access

payout issues

refund struggles

weak or vanishing support

business conduct serious enough to produce a published federal appellate case

Trust the Pattern More Than the Pitch

In the online world, polished presentations are easy to create. A smooth website, persuasive webinar, confident language, and carefully chosen testimonials can make almost anything appear credible for a moment. First impressions, especially when professionally packaged, can be remarkably persuasive.

But what matters most is rarely the front-end experience. It is what happens after payment that reveals the true nature of a business.

Does support remain available when questions arise, or does communication suddenly become difficult? Is access delivered as promised, or quietly restricted once the transaction is complete? Are refunds handled fairly and professionally, or turned into a prolonged struggle? Are payouts honored consistently, or delayed, disputed, and withheld when it matters most?

These moments are not minor details. They are often the clearest indicators of integrity. Anyone can design an appealing pitch. Far fewer can sustain trust once money has changed hands.

When support disappears, access is cut, refunds become exhausting battles, or payouts fail to arrive, the original sales message begins to reveal itself for what it may have been: not the truth, but the hook.

That is why wise consumers learn to study patterns rather than promises. A persuasive pitch can last an hour. A business pattern can speak for years.

The most important question is not how impressive something sounds before you join. It is how people are treated after they have paid, when the spotlight is gone and the marketing has done its job.

Trust is not proven in the presentation. It is proven in the follow-through.

Why Our Definition of “Due Diligence” Has to Change

There was a time when many people believed they had done enough research if a webinar looked professional, if the presenter sounded knowledgeable, or if the opportunity had been recommended by someone they already trusted. A polished sales page, a confident voice, and a familiar endorsement were often enough to create a sense of reassurance. For many years, that was how countless people judged whether something seemed legitimate.

Today, that standard is no longer sufficient.

The online world has evolved, and so have the methods used to persuade people. Sophisticated branding, attractive websites, smooth presentations, and carefully crafted testimonials can now be created with remarkable ease. What once appeared to be a sign of credibility may simply be a sign that someone understands marketing well. Those are not always the same thing.

Real due diligence now requires a deeper and more thoughtful approach. It means taking the time to look beyond the presentation and into the substance of what is being offered. It means searching public records when appropriate, reading independent reviews, paying attention to patterns of unresolved complaints, and noticing whether names, brands, or programs seem to change frequently whenever criticism begins to surface. It also means asking an often-overlooked question: what happens to customers after they have paid?

That final question can reveal more than any sales webinar ever could.

How a business treats people once the transaction is complete often tells the real story. Are customers supported when problems arise? Are refund policies honored fairly? Are questions answered respectfully? Do people feel helped, or simply processed and forgotten? These are the details that separate genuine businesses from operations built primarily on acquisition rather than service.

This shift in how we think about due diligence matters because many modern scams no longer look careless or obvious. They often appear polished, upscale, and convincing. They may borrow the language of success, community, mentorship, and opportunity. They may look far more sophisticated than the stereotypes people still imagine when they hear the word scam.

Yet appearance alone has never been evidence.

A beautiful presentation can be designed in a weekend. A compelling pitch can be rehearsed. Testimonials can be curated. Social proof can be manufactured. None of those things automatically confirm integrity.

What tends to matter far more is the paper trail left behind: court records, complaint histories, repeated patterns, broken promises, and the experiences of those who came before you.

In a world where image can be created quickly, substance remains slower, quieter, and infinitely more valuable.

Practical Reminders to Help You Avoid Falling Prey to Scammers Like Jordon Schultz

Research the people behind the opportunity and its leadership before investing your trust. A polished brand can be built quickly, but character usually reveals itself over time. Take the time to learn who is leading the company, how they have treated others, and what kind of reputation follows them.

Look beyond the sales page and into the real story. Search for public records, complaints, past ventures, unresolved disputes, and the experiences of those who came before you. What is hidden in the background often matters more than what is shining in the foreground.

Be cautious whenever urgency replaces clarity. Pressure to act quickly, limited-time language, or the feeling that you must decide immediately are often signs to slow down rather than speed up. Opportunities built on truth can withstand reflection.

Keep records of what was promised. Save screenshots, emails, presentations, and written claims before joining anything. Memory fades, but documentation brings clarity when confusion begins.

Pay attention to how people are treated after they join. Anyone can be warm and persuasive before payment. The real measure of a business is how it responds when questions arise, support is needed, or challenges appear.

Trust patterns more than presentations. A single charming pitch can be rehearsed. A repeated pattern tells the deeper truth. When similar concerns keep surfacing from different people over time, it is wise to pay attention.

Never hand over your peace of mind for the promise of easy success. If something feels rushed, murky, overly complicated, or ethically uncomfortable, honor that instinct. Peace, integrity, and self-respect are worth far more than any shiny opportunity.

Final Verdict on Jordon Schultz

After reviewing the federal bankruptcy case, the appellate outcome, the documented valuation dispute, and the broader pattern of complaints that continue to surround his name, my honest view is simple: Jordon Schultz is not someone I would trust with my money, my time, or my future.

This was not just a case of one unhappy customer or a misunderstood business disagreement. It became a published federal appellate matter with serious consequences, including the denial of his bankruptcy discharge under § 727(a)(7). That alone places this situation far beyond ordinary online criticism or casual internet gossip.

Just as importantly, the heart of the case was credibility.

When someone publicly describes an asset as being worth $1 million, then schedules it at $348.60 in sworn bankruptcy filings, reasonable people are entitled to ask serious questions. And when those questions end in a court ruling that survives appeal, those concerns do not simply disappear with time.

When that legal history is viewed alongside repeated complaints involving aggressive sales tactics, hidden costs, blocked payouts, refund problems, disappearing support, and rebranded offers, the overall picture becomes difficult to ignore.

My final verdict: there are far too many warning signs here for anyone to proceed casually. There are too many ethical educators, honest business opportunities, and transparent mentors available online to gamble on a track record like this.

Legitimate Alternatives to Make Money Online

One of the hardest parts after reading about a scammer like Jordon Schultz is that people can begin to doubt everything online. That reaction is understandable, but it is not entirely accurate.

There are legitimate ways to make money online. There are real platforms, ethical business models, and genuine opportunities that reward skill, consistency, patience, and effort. The key difference is that real opportunities do not rely on secrecy, unrealistic guarantees, or pressure tactics. They are built on value creation, transparency, and results that come through action over time.

That is also why I take recommendations seriously.

I do not believe in promoting random platforms I have never touched, nor repeating hype just because something is trending. I only recommend opportunities I have personally researched, signed up for, tested, applied, and gained real experience with myself.

My approach is simple:

Research the company, model, and leadership

Join and test the platform firsthand

Apply the methods consistently

Evaluate the real user experience

Review the results honestly — good or bad

Recommend only what I genuinely stand behind

I believe that is the only responsible way to speak about making money online.

Too many people online criticize or promote opportunities they have never even used. That creates noise, confusion, and unnecessary negativity. My preference is a more grounded and unbiased approach: test first, speak second, and take responsibility for your own choices. Even when something does not turn out to be a success, you have still invested in your own learning and experience.

If something does not work out for me, I am honest about it. But I do not bash the person who recommended it, because ultimately the decision was mine. Building any business takes time, resources, effort, and money. If you do not have enough of those available, I do not recommend pursuing these kinds of opportunities in the first place.

Never invest in something you cannot afford to lose, and never shift responsibility onto others for a decision you chose to make yourself.

Sometimes the best path forward after disappointment is not to give up, but it is simply to choose wiser, do your own research first, get facts and proof, and pick more transparent opportunities next time.

Resources and Recommended Reading

When stories like this surface, it is easy to focus only on one person or one program. But the wiser path is to use situations like this as an opportunity to become stronger, sharper, and more informed for the future.

That is why I always recommend combining practical consumer resources with books that improve judgment, discernment, and decision-making. Protecting yourself is not only about reacting after something goes wrong — it is about learning how to spot warning signs earlier next time.

The FTC is one of the best places to learn how scams operate, how to report deceptive business practices, and how to recognize common fraud tactics before they cost you money.