Article At A Glance: Aintuition Platform Review

- Aintuition was not an AI investment platform — it was a crypto Ponzi scheme that collapsed in March 2026 after disabling withdrawals and disappearing with an estimated $30 million in investor funds.

- The platform was fronted by an anonymous masked character called “Mr. Klaus,” a Russian figure who never revealed his real identity — a massive red flag that was ignored by thousands of depositors.

- Before collapsing, Aintuition attracted around 75,700 monthly website visitors from the US, Belgium, Germany, and Australia — meaning the damage was widespread and international.

- The platform’s final move was aggressively pushing “critical 24-hour investment plans” the day before shutting down withdrawals — a classic last-ditch Ponzi cash grab.

- Keep reading to understand exactly how the scam worked, the warning signs that were hiding in plain sight, and how to protect yourself from the next version of this same playbook.

Aintuition collapsed almost overnight — and thousands of people lost real money before anyone sounded the alarm loud enough.

For those who found this review while researching the platform, here is the short version: Aintuition was a fraudulent MLM crypto Ponzi scheme disguised as an AI-powered investment platform. It promised daily returns, used recruitment-based income structures, and was run by an anonymous masked figure who called himself “Mr. Klaus.” By March 24, 2026, the whole operation had imploded, withdrawals were frozen, and the official explanation was a story about losing $30 million in a casino deal gone wrong. The website was disabled entirely by March 25th. Understanding how and why this happened matters — not just for victims, but for anyone navigating the increasingly crowded world of AI and crypto investment claims. BehindMLM, which covers MLM and crypto fraud extensively, was one of the first outlets to flag Aintuition back in February 2026.

Aintuition Was Never a Real AI Investment Platform

The name “Aintuition” was designed to sound like a fusion of artificial intelligence and financial intuition — a clever branding choice that gave the platform a veneer of technological credibility. But there was no underlying AI system generating returns. There was no proprietary trading algorithm, no verifiable technology stack, and no audited financial disclosures. It was a name built to attract people excited about AI without giving them anything real to hold onto.

Real AI investment platforms — the legitimate ones — are registered financial entities with regulatory oversight, audited returns, and transparent leadership. Aintuition had none of these. What it had instead was polished marketing, a slick dashboard, and a charismatic anonymous figurehead designed to project authority without accountability.

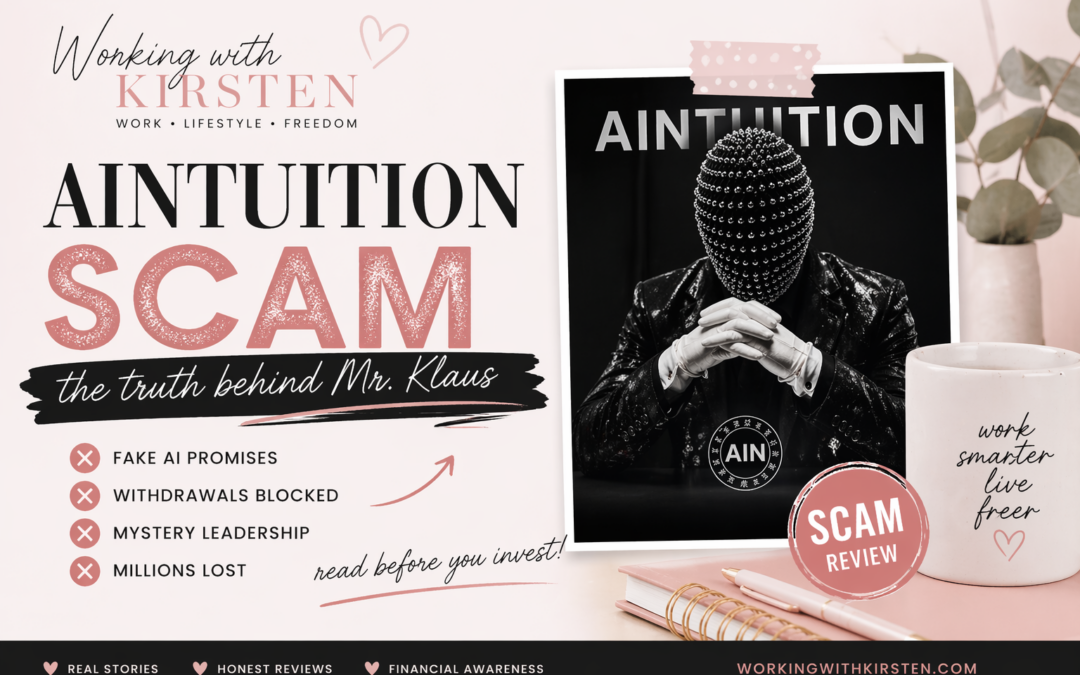

The “Mr. Klaus” Masked Figurehead and Russian Origins

Instead of a CEO with a verifiable professional history, Aintuition gave investors a Russian man in a spiky gimp mask who went by “Mr. Klaus.” He appeared in promotional videos, fronted webinars, and acted as the public face of the operation. His real identity was never disclosed. On March 24th — the day after withdrawals were disabled — Mr. Klaus appeared in a marketing webinar where he apologized for withdrawal delays and claimed they would be resolved within five business days. That promise was never kept.

The Daily Returns Promise That Should Have Been a Red Flag

Aintuition promoted investment plans built around consistent daily returns. Any platform promising guaranteed daily percentage gains on crypto deposits is, by definition, not generating those returns through legitimate trading or AI activity. Sustainable daily returns at those levels are mathematically impossible to maintain without a constant inflow of new capital — which is exactly the definition of a Ponzi scheme. This single detail alone should have stopped every deposit before it started.

How the Fake Dashboard Created False Profit Illusions

Like most Ponzi operations, Aintuition used an investor dashboard that displayed growing balances and apparent profits. These numbers were not real. They were fabricated figures meant to create a psychological sense of success and encourage larger deposits. When users tried to withdraw those “profits,” that’s when the system’s true nature became visible — fees, delays, and eventually a complete lockout. The dashboard was a retention tool, not a financial record. For more details on the collapse of Aintuition, you can read this article on Aintuition’s collapse.

How the Aintuition Scam Actually Worked

At its core, Aintuition operated on a model where money coming in from new investors was used to pay older investors their promised returns. There was no external revenue source. No casino profits, no AI trading wins, no legitimate business income. The entire financial engine ran on recruitment and fresh deposits — and the moment those slowed down, the collapse was inevitable.

The MLM Crypto Ponzi Structure Explained Simply

Aintuition layered a multi-level marketing structure on top of its Ponzi mechanics. Investors were incentivized to recruit others, earning commissions when their referrals deposited funds. This kept the money flowing upward and outward without requiring Aintuition to generate any real returns. The MLM layer also created a community of motivated promoters who genuinely believed in the platform — not because it was legitimate, but because their own commissions depended on its continued growth.

Why New Investor Money Was the Only Real Revenue

This is the fundamental truth behind every Ponzi: the only money in the system is the money investors put in. Aintuition had no other income stream. Every withdrawal paid out to an early investor came directly from a later investor’s deposit. When new deposits slowed — as they always eventually do — the system ran out of cash to pay withdrawals, and the operators made their exit.

The Withdrawal Trap: Fake Fees to Extract More Money

A particularly predatory tactic used by Aintuition involved withdrawal fees. When investors tried to access their funds, they were told they needed to pay additional fees before their withdrawals could be processed. This is a well-documented exit scam technique — it extracts one final payment from victims at the most desperate moment, right when they’re trying to recover their money. Those fees were never returned, and the withdrawals never came through.

The Final 48 Hours Before Aintuition Collapsed

The 48-hour window between March 22nd and March 24th, 2026 was a masterclass in how Ponzi schemes execute their exit. The moves were calculated, the messaging was deliberately vague, and the timeline was compressed enough that most investors didn’t have time to react before their funds were already unreachable.

The Suspicious “Critical 24-Hour Investment Plans” Push on March 22

On March 22nd, 2026 — just one day before withdrawals were disabled — Aintuition launched an aggressive promotional push for what they called “critical 24-hour investment plans.” This kind of language is not accidental. Urgency-based investment pushes in the final hours of a Ponzi scheme are a deliberate cash extraction strategy. The operators knew the end was coming and used manufactured FOMO to squeeze as many last-minute deposits as possible from both new and existing investors before pulling the plug.

Withdrawals Disabled on March 23, 2026

On March 23rd, Aintuition quietly disabled all withdrawals. No advance notice. No explanation at the time. Investors who tried to access their funds were simply locked out. For most, this was the first sign that something was catastrophically wrong — even though the warning signs had been present for weeks.

The silence on March 23rd was strategic. By saying nothing initially, Aintuition bought itself roughly 24 hours before panic fully set in. That window gave the operators time to prepare their exit narrative, close down communication channels, and get their story straight before the questions became impossible to ignore.

The $30 Million Casino Deal Excuse

When Aintuition finally broke its silence on March 24th, the explanation it offered was extraordinary. According to the platform’s official statement, Aintuition had taken approximately $30 million in investor funds and used them to acquire a casino — and the deal had gone sideways due to fraud. The money was gone. Systems were compromised. Support was down. It was a narrative so absurd it almost seemed designed to insult the intelligence of its victims. No legitimate investment platform moves all investor capital into a single undisclosed casino acquisition without investor consent. The “casino fraud” story was an exit-scam cover, nothing more.

Who Lost Money and How Much Was at Stake

The scale of Aintuition’s reach before its collapse was significant. This was not a small operation targeting a niche audience. It had real traffic, real depositors across multiple countries, and a polished enough presentation to convince tens of thousands of people it was worth trusting with their money. The human cost behind the traffic numbers is the part that gets lost in the coverage of how cleverly the scam was structured.

75,700 Monthly Website Visitors Before Collapse

In the month leading up to its collapse, SimilarWeb recorded approximately 75,700 monthly visits to Aintuition’s website. That figure represents a substantial audience actively engaging with the platform — researching plans, logging into dashboards, or depositing funds. For context, that level of traffic puts Aintuition well above most legitimate early-stage fintech startups in terms of visibility.

Traffic volume does not equal legitimacy, but it does reflect the scale of potential victims. If even a fraction of those monthly visitors were active depositors, the total funds at risk were enormous. The $30 million figure cited in Aintuition’s own exit statement gives some indication of how much capital had actually been collected before the shutdown.

Top Victim Countries: US, Belgium, Germany and Australia

Aintuition’s reach was international, with its largest audiences concentrated in four countries. The geographic spread tells an important story — this was not a regional scam targeting one language group or one economic market. It was a multilingual, multi-market operation with the infrastructure to attract investors across different time zones and regulatory environments.

The presence of US, Belgian, German, and Australian victims is also significant from a regulatory standpoint. Each of these countries has active financial regulators — the SEC, FSMA, BaFin, and ASIC respectively — and none of them appear to have flagged Aintuition before the collapse occurred. That gap highlights how quickly these operations can scale before oversight catches up.

For victims in these countries, recovery options are limited but not entirely nonexistent. Reporting to national financial regulators, filing with local consumer protection agencies, and documenting all transaction records are the recommended first steps — though the realistic chance of fund recovery from a collapsed Ponzi is, unfortunately, very low.

- United States — Largest traffic source; victims can report to the SEC at sec.gov/tcr or the FTC at reportfraud.ftc.gov

- Belgium — Second largest source; the Financial Services and Markets Authority (FSMA) handles crypto fraud complaints

- Germany — BaFin is the relevant authority; complaints can be submitted directly through their consumer portal

- Australia — ASIC manages investment fraud reports; victims can also contact the Australian Cyber Security Centre for crypto-specific cases

Aintuition’s Trustpilot Ratings Tell the Real Story

Aintuition held a TrustScore of 2.0 out of 5 on Trustpilot — a “Poor” rating that reflected what depositors actually experienced once they tried to interact with the platform beyond the initial deposit stage. A 2.0 score on Trustpilot for a financial platform is not a minor concern. It is a documented trail of user complaints that anyone could have found before depositing a single dollar.

The pattern in low-rated reviews for platforms like Aintuition is almost always the same: glowing early reviews (often fake or incentivized), followed by a growing wave of complaints about withdrawal issues, unresponsive support, and disappearing funds. By the time the negative reviews dominate the page, the operators are already preparing their exit. Trustpilot scores for investment platforms deserve more weight than most people give them during the research phase.

It is worth noting that some positive Trustpilot reviews for Aintuition were almost certainly fabricated or posted by affiliates who were earning MLM commissions. Recruited promoters have a financial incentive to generate positive social proof, which is why review platforms alone cannot be the only due diligence tool — but a 2.0 average means the authentic negative experiences were strong enough to drag the score down despite any artificial inflation.

🌿Let’s Stay Connected & Continue the Conversation…

If reflections like this resonate with you, you may enjoy the Working With Kirsten newsletter, where I occasionally share deeper thoughts about building a meaningful online lifestyle, navigating digital communities, and creating environments that encourage curiosity and personal growth.

Inside the newsletter, I often expand on many of the themes explored here on the blog — including the evolving culture of the online world, the importance of thoughtful communities, and the small habits that quietly shape how life feels from day to day.

✨ Reflections on building a thoughtful internet lifestyle

🌱 Insights on personal growth and digital communities

☕ Behind-the-scenes perspectives from my own journey online

If these ideas interest you, you’re always welcome to join the conversation.

Join the Newsletter – Click Here!

No noise. Just thoughtful ideas and quiet reflections about building a life that feels genuinely rich.

How to Spot the Next Aintuition Before You Lose Money

Aintuition is gone, but the template it used is not. The same structure — anonymous founders, AI branding, guaranteed daily returns, MLM recruitment layers, fake dashboards, and manufactured urgency — gets recycled into new platforms constantly. The names change. The masks change. The mechanics do not.

The most effective defense is pattern recognition. Knowing what a Ponzi looks like in its growth phase — before the collapse, not after — is the only way to avoid becoming a statistic in the next post-mortem review. The warning signs are rarely hidden. They are just easy to rationalize away when a platform appears to be generating profits on your dashboard.

Here is a direct comparison between what a legitimate AI investment platform looks like versus what Aintuition offered:

Feature Legitimate Platform Aintuition Leadership Named, verifiable CEO with public history Anonymous “Mr. Klaus” in a mask Returns Variable, market-dependent, disclosed risk Guaranteed daily returns (unsustainable) Revenue Source Documented, audited business activity New investor deposits only Withdrawals Processed on demand, no surprise fees Blocked, fee-gated, then disabled entirely Regulation Registered with financial authorities No registration, no oversight Trustpilot Score 4.0+ with verified reviews 2.0 — rated Poor

If a platform you are researching matches even two or three of the Aintuition column entries above, stop. Do not deposit. Move on.

1. Guaranteed Daily Returns Above 1% Are Always a Lie

No legitimate investment vehicle — AI-powered or otherwise — can guarantee consistent daily returns. Markets are volatile. Algorithms have drawdown periods. Any platform promising fixed daily percentage gains is either lying about its returns or running a Ponzi structure where your profits are being funded by someone else’s deposit. The math does not work any other way. When a platform guarantees returns, it is not offering you an investment. It is offering you a trap.

2. Anonymous Founders Are a Non-Negotiable Red Flag

Anonymity in a financial platform is not a feature — it is a liability shield. When founders cannot be identified, they cannot be held accountable. “Mr. Klaus” was never going to face consequences because no one knew who he was. Before depositing money into any platform, search for the named leadership team on LinkedIn, cross-reference their claimed credentials, and verify that they have a documented professional history. If the founder is masked, fictional, or simply absent from the about page, walk away immediately.

3. Withdrawal Fees After Deposit Are a Classic Exit Scam Tactic

Legitimate investment platforms do not charge fees to release your own money. When Aintuition began blocking withdrawals and demanding additional payments before funds could be released, that was not a technical glitch or a compliance procedure — it was a deliberate extraction tactic. The fee-before-withdrawal mechanic is one of the oldest tricks in the exit scam handbook. It exploits the sunk cost fallacy: investors who have already deposited significant funds are psychologically primed to pay a little more if they believe it will unlock what they are owed. It never does.

4. Pressure Tactics and “Limited Time” Investment Windows Signal Collapse

When Aintuition launched its “critical 24-hour investment plans” on March 22nd, it was not running a promotion. It was running out of time. Manufactured urgency — countdown timers, limited availability windows, “act now” language — is almost always a signal that a Ponzi operator is making their final cash sweep before shutting everything down. Legitimate investment platforms do not pressure you to deposit within 24 hours. They do not frame missing an investment window as a financial emergency. Any platform that creates that kind of pressure is not trying to help you grow wealth. It is trying to take what you have before you figure out what is happening.

Aintuition Is Gone, But the Playbook Gets Recycled

The Aintuition collapse followed a script that has been used dozens of times before — and will be used dozens of times again. The specific details shift: the AI angle replaces a forex trading angle, the spiky mask replaces a stock photo CEO, the casino fraud story replaces a hacking incident. But the underlying mechanics are identical every single time. Money comes in from new investors, early investors get paid to generate testimonials and referrals, the dashboard shows fake profits, withdrawals get quietly gated, and then one final urgency push extracts the last round of deposits before the whole thing goes dark. The people running these operations are not improvising. They are following a tested, repeatable model that keeps working because enough people do not recognize it until it is too late. The best protection is not better regulators or smarter algorithms — it is understanding the pattern well enough to spot it in its growth phase, before the collapse, when the platform still looks like it might be real.

Everything that mattered pointed in the same direction: anonymous leadership, guaranteed daily returns, recruitment incentives, fake-looking dashboard growth, withdrawal problems, surprise fees, and finally a complete collapse once new money slowed down. Those are not isolated concerns — they are the standard fingerprints of a fraudulent operation.

The masked persona of “Mr. Klaus” may have created mystery and intrigue for some, but in finance, anonymity should never replace accountability. If people are asking you to trust them with money while refusing to reveal who they are, that alone should end the conversation.

The most painful part is that many victims were not reckless people. They were ordinary individuals looking for opportunity, security, or a better future. Scams like Aintuition succeed because they package hope in a convincing format.

My final verdict is simple: Aintuition was a scam, not an investment. It used the language of innovation to hide the mechanics of exploitation.

And while Aintuition is gone, the next version is likely already being built under a different name.

That is why this story matters.

Not to shame victims.

Not to sensationalize losses.

But to help more people recognize the pattern before they deposit into the next polished illusion.

If one person reads this article and avoids losing money to the next “AI wealth platform,” then exposing what happened here was worth it.

Resources & Recommended Reading

If the Aintuition collapse taught us anything, it is that financial education matters just as much as financial opportunity. Many scams succeed not because people are foolish, but because they are navigating complex markets filled with polished promises, urgency tactics, and language designed to confuse rather than clarify.

The best defense is not fear — it is knowledge.

Below are resources and books worth exploring if you want to better understand investing, psychology, scams, and how to protect yourself in a world where hype often moves faster than truth.

Understanding How Scams Persuade Smart People

1. The Confidence Game by Maria Konnikova

A powerful look at why intelligent, capable people fall for fraud — and how con artists build trust before they steal it.

Why I recommend reading it:

This book helps you understand that scams are rarely about intelligence. They are about psychology, timing, emotion, and manipulation. It can remove shame while sharpening awareness.

2. Influence: The Psychology of Persuasion by Robert Cialdini

Essential reading for understanding urgency, authority, scarcity, and the persuasion triggers commonly used in scams.

Why I recommend reading it:

Once you understand persuasion tactics, you begin to recognize them everywhere — from scam offers to aggressive sales funnels and misleading marketing.

Learning Real Investing Principles

3. The Little Book of Common Sense Investing by John C. Bogle

A grounded reminder that long-term wealth is usually built through patience, diversification, and realism — not miracle returns.

Why I recommend reading it:

This is the perfect antidote to “get rich quick” thinking. It brings you back to timeless principles that have created wealth for ordinary people over decades.

4. The Psychology of Money by Morgan Housel

One of the best modern books on how emotions, behavior, and decision-making shape financial outcomes more than flashy strategies.

Why I recommend reading it:

Many poor financial decisions are emotional, not mathematical. This book helps you understand patience, risk, ego, and why mindset often matters more than tactics.

Understanding Fraud and Financial Crime

5. Billion Dollar Whale by Tom Wright and Bradley Hope

A gripping true story of large-scale deception and how image, influence, and complexity can hide fraud in plain sight.

Why I recommend reading it:

This book shows how fraud can thrive at the highest levels of business, politics, and finance. It is a reminder that size, prestige, and media attention do not equal legitimacy.

6. Bad Blood by John Carreyrou

Not a crypto story, but an important case study in how hype and secrecy can overpower scrutiny for years.

Why I recommend reading it:

This is one of the best examples of how charisma, branding, and fear of missing out can silence common sense. It teaches the importance of asking hard questions before trusting bold claims.

Practical Consumer Protection Resources

Useful for reporting fraud and learning common scam tactics.

U.S. Securities and Exchange Commission

Helpful for understanding registered investments and reporting suspicious offerings.

Excellent public warning lists and scam education resources.

When you educate yourself after being scammed—or to prevent it from happening in the first place—the goal is not to become cynical. It is to become discerning.

There are real opportunities in the world, but they rarely arrive wearing masks, promising guaranteed daily returns, and demanding urgency-driven deposits.

Slow wisdom usually beats fast promises but it takes time and patience like anything good in life.

You can also check out some of my other articles I recently wrote about recent other scams to further your education. Make sure to run for the hills when you hear the name Bobby Jones, Cliqly, Clickerr, or Push Platform. Check out my latest Bobby Jones Scam Push Platform article right here!

Conclusion

The collapse of Aintuition is a reminder that scams evolve faster than many people realize. They borrow whatever language is trending, wrap themselves in modern design, and present old fraud models as new opportunities. Yesterday it was forex. Today it is AI. Tomorrow it will be something else.

But while the branding changes, the warning signs stay remarkably consistent: anonymous leadership, unrealistic returns, pressure to act quickly, recruitment-driven growth, and excuses when withdrawals stop.

What happened with Aintuition was unfortunate, but it can also be educational. Every exposed scheme gives people a clearer lens for spotting the next one earlier. That knowledge has value. It protects savings, time, trust, and emotional wellbeing.

For those who lost money, the lesson is not that you failed. The lesson is that deception can be sophisticated, persuasive, and emotionally targeted. Many capable people have been caught in similar traps. What matters now is what comes next: documenting what happened, reporting it where possible, and moving forward wiser than before.

For everyone else, let this be a reminder that real wealth is rarely built through secrecy, urgency, or guaranteed returns. It is usually built through patience, transparency, steady decision-making, and strategies that still make sense when the excitement fades.

Aintuition may be gone, but the deeper lesson remains:

If an opportunity needs confusion to survive, it was never an opportunity at all.

Frequently Asked Questions

These are the most common questions being asked about Aintuition following its collapse in March 2026. The answers below are based on documented events and verified reporting.

Was Aintuition a Legitimate AI Company?

No. Aintuition was not a legitimate AI company. It used AI-themed branding to appear credible, but there was no documented artificial intelligence technology behind the platform, no verifiable trading algorithm, and no audited financial activity that would support the returns it promised.

The platform was classified by independent MLM and fraud analysts as a crypto Ponzi scheme with a multi-level marketing recruitment layer. Its business model relied entirely on new investor deposits to pay existing investors — which is the defining characteristic of a Ponzi, not an AI investment platform.

Can Aintuition Victims Recover Their Money?

Recovery is extremely difficult in collapsed Ponzi schemes, and Aintuition’s rapid website shutdown as of March 25th, 2026 makes it even harder. The operators are anonymous, the funds have likely been moved through crypto wallets that obscure their trail, and there is no registered legal entity to pursue through civil litigation. Victims should report to their national financial regulator immediately, preserve all transaction records, and consult with a financial fraud attorney, but they should go in with realistic expectations. The honest answer is that most victims of collapsed crypto Ponzis recover little to nothing.

What Was the $30 Million Casino Deal Aintuition Claimed?

On March 24th, 2026, Aintuition issued an official statement claiming that investor funds — approximately $30 million — had been used to acquire a casino, and that the deal had been compromised by fraud, resulting in the loss of those funds. The statement was widely interpreted by fraud analysts as a fabricated exit narrative.

No evidence of a legitimate casino acquisition was ever provided. No legal documentation, no named casino, no third-party verification. The timing alone — this explanation arriving less than 48 hours after withdrawals were disabled, on the same day the YouTube channel was closed — points strongly to a constructed alibi rather than a genuine business disaster. Moving all investor funds into a single undisclosed acquisition without consent would itself be a serious legal violation in any regulated jurisdiction.

Who Was “Mr. Klaus” Behind Aintuition?

“Mr. Klaus” was the masked, anonymous figurehead who served as Aintuition’s public face. He appeared in promotional videos and webinars wearing a distinctive spiky mask and was identified as Russian-speaking based on his recorded communications. His real identity was never disclosed, and no verified personal information about him has surfaced following the collapse.

Detail What Was Known Real Name Unknown — never disclosed Nationality Identified as Russian-speaking Public Appearance Wore a spiky mask in all video content Last Known Activity March 24th webinar apologizing for withdrawal delays Current Status No public communications since collapse; whereabouts unknown

The use of a mask and pseudonym was not an aesthetic choice — it was a deliberate anonymity strategy. By ensuring he could never be personally identified, “Mr. Klaus” built himself a complete shield against legal accountability. Investors had no way to name him in a complaint, no way to verify his credentials, and no way to find him after the platform went dark.

This is why anonymous leadership is one of the most important red flags in evaluating any investment platform. The mask was not a quirky marketing gimmick. It was an exit plan built into the brand from day one.

How Do I Report a Crypto Ponzi Scheme Like Aintuition?

If you deposited funds into Aintuition or a similar platform, reporting to the appropriate authorities is the most important step you can take — both for your own case and to help prevent others from being victimized by rebranded versions of the same operation.

Before filing any report, gather and preserve the following documentation: all deposit transaction records and wallet addresses, screenshots of your dashboard showing promised returns, any communications you received from the platform (emails, Telegram messages, webinar recordings), and records of any fees you were charged during withdrawal attempts. The more documentation you have, the stronger your report will be.

Depending on your country, here are the relevant reporting channels:

Country Reporting Authority Where to Report United States SEC / FTC / FBI IC3 sec.gov/tcr — reportfraud.ftc.gov — ic3.gov Belgium FSMA fsma.be/en/complaints Germany BaFin bafin.de/EN/Verbraucher/consumer_node.html Australia ASIC / ACSC asic.gov.au/report — cyber.gov.au/report All Countries Interpol Financial Crimes interpol.int/en/Crimes/Financial-crime

Beyond formal reporting, sharing your experience on verified consumer platforms like Trustpilot, filing a warning with BehindMLM, and alerting your local news or consumer protection organizations all contribute to a public record that makes it harder for the same operators to relaunch under a new name.

If you are unsure whether a platform you are currently using shares characteristics with Aintuition, use the comparison table earlier in this article as a reference checklist — and remember that the most reliable rule remains the simplest one: if it guarantees daily returns and the founder is wearing a mask, it is not an investment. It is a countdown.

Share Your Perspective: Have You Been Scammed by Aintuition?

🌿Let’s Stay Connected & Continue the Conversation…

If reflections like this resonate with you, you may enjoy the Working With Kirsten newsletter, where I occasionally share deeper thoughts about building a meaningful online lifestyle, navigating digital communities, and creating environments that encourage curiosity and personal growth.

Inside the newsletter, I often expand on many of the themes explored here on the blog — including the evolving culture of the online world, the importance of thoughtful communities, and the small habits that quietly shape how life feels from day to day.

✨ Reflections on building a thoughtful internet lifestyle

🌱 Insights on personal growth and digital communities

☕ Behind-the-scenes perspectives from my own journey online

If these ideas interest you, you’re always welcome to join the conversation.

Join the Newsletter – Click Here!

No noise. Just thoughtful ideas and quiet reflections about building a life that feels genuinely rich.

Disclosure

Some of the links in this article may be affiliate links. This means that if you choose to make a purchase through one of these links, I may earn a small commission at no additional cost to you.

I only recommend books, services, products, tools, or communities that I genuinely find interesting, useful, or aligned with the ideas discussed on this site and that I am using myself.

My goal with WorkingWithKirsten.com is to explore thoughtful perspectives on online culture, digital entrepreneurship, and building a more intentional internet lifestyle. Any resources mentioned are shared with the intention of helping readers explore these topics further.

Thank you for supporting this work and for being part of the conversation.

Hi, I’m Kirsten!

I started Working with Kirsten to share my journey of rebuilding from burnout, scams, and setbacks — and to help others create purpose-driven income online.

Over the years, I’ve explored nearly every online business model you can think of — eBay, Amazon, Kindle publishing, Etsy, eCommerce — chasing freedom, creativity, and stability. Some of it worked. Some of it didn’t. I eventually burned out hard after losing my Kindle account, and later, I hit rock bottom when I was caught in one of the biggest affiliate scams of 2024, losing over $14,000 in unpaid earnings.

That moment nearly ended everything.

But instead of giving up, I used what I’d learned to rebuild. I found my mentor, tapped back into my creative energy, and started building a business that actually felt good to run — not just profitable, but meaningful.

That’s how Working with Kirsten and my philosophy of Helponomics were born — the idea that by helping others first, success naturally follows.

Today, I’m a digital creator and affiliate marketer focused on ethical partnerships, aligned offers, and creating income that’s both sustainable and soul-led.

Whether you’re just starting out or starting over, I’m here to show you that you don’t need to hustle yourself into exhaustion or fall for the hype. You can build a business with purpose, resilience, and heart — and I’d love to help guide you every step of the way.